Many economists believe the Reserve Bank will start cutting interest rates in the final quarter of 2024. So if you’re thinking about entering the market, should you buy now or wait for those potential rate cuts to occur?

To answer that question, it can be helpful to consult long-term data. During the decade to January 2024, Australia’s median property rose 80.1%, according to PropTrack. Prices rose faster in the combined regions than the combined capital cities (92.5% vs 75.7%), while house growth exceeded unit growth (89.4% v 44.4%). But the general trend for all these categories was the same – up.

Domain’s chief of research & economics, Nicola Powell, believes buyers should take a longer-term view and not get too hung up about how the market is currently performing.

“When you’re purchasing a property, it’s for a long-term investment and you are going to ride multiple property cycles, and that’s how you build financial wealth. So if I would give any advice, it would be to buy when it’s right for you. Housing markets are complex and often impossible to predict.”

Ultimately, the question or whether to buy now depends on your personal situation and goals. For some, now will be the right time; for others, it will be better to wait. We’re happy to have a chat and run the numbers for you, so we can present personalised loan options for your situation.

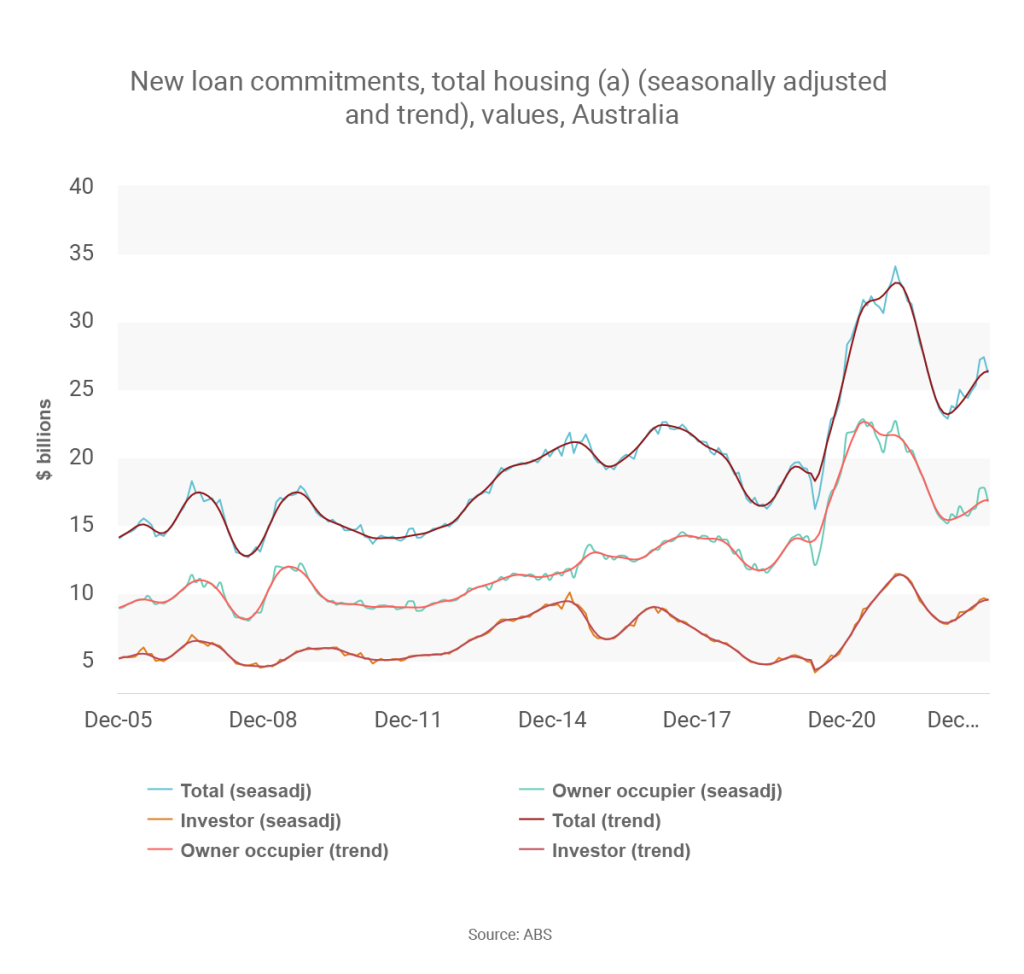

First home buyer loans rise 12.9%

There’s been a significant increase in first home buyer activity over the past year, based on the latest data from the Australian Bureau of Statistics.

There were a total of 9,491 owner-occupier first home buyer mortgages issued across Australia in December 2023, which was 12.9% higher than the year before.

First home buyer activity rose in six of the eight states and territories, with Queensland and Tasmania being the exceptions to the rule.

While it can be challenging to buy your first home, this data shows it’s not impossible. Here are four tips to get on the property ladder:

- Look for ways to decrease your spending

- Check whether you’re eligible for the First Home Guarantee or Regional First Home Buyer Guarantee

- Consider asking your parents or another relative to guarantee your home loan (so you can drastically reduce or even eliminate your deposit requirement)

Contact us, so we can explain your options and coach you through the process.

50% of borrowers may not understand lender’s mortgage insurance

A significant number of borrowers are unclear about lender’s mortgage insurance (LMI), according to a recent survey of mortgage brokers by LMI provider Helia.

The survey found that 85% of broker respondents think LMI can benefit buyers who want to get into the market earlier, while 70% believe it can also help renters who want to transition into ownership. However, 50% of respondents feel borrowers generally don’t properly understand LMI.

LMI is a form of insurance that protects the lender in case the borrower defaults on the mortgage and the lender can’t recover the loan from selling the home. The premium varies, depending on the size, type and location of the property.

Lenders generally insist borrowers take out LMI if they want to buy a property with less than a 20% deposit – although, for some professions, such as doctors and lawyers, it’s possible to buy a property with a smaller deposit without paying LMI.

The upside to using LMI is you can enter the market with a smaller deposit; the downside is the cost.

We’d be happy to discuss both the potential benefits and costs, so you can make an informed decision about whether LMI is right for your personal situation.

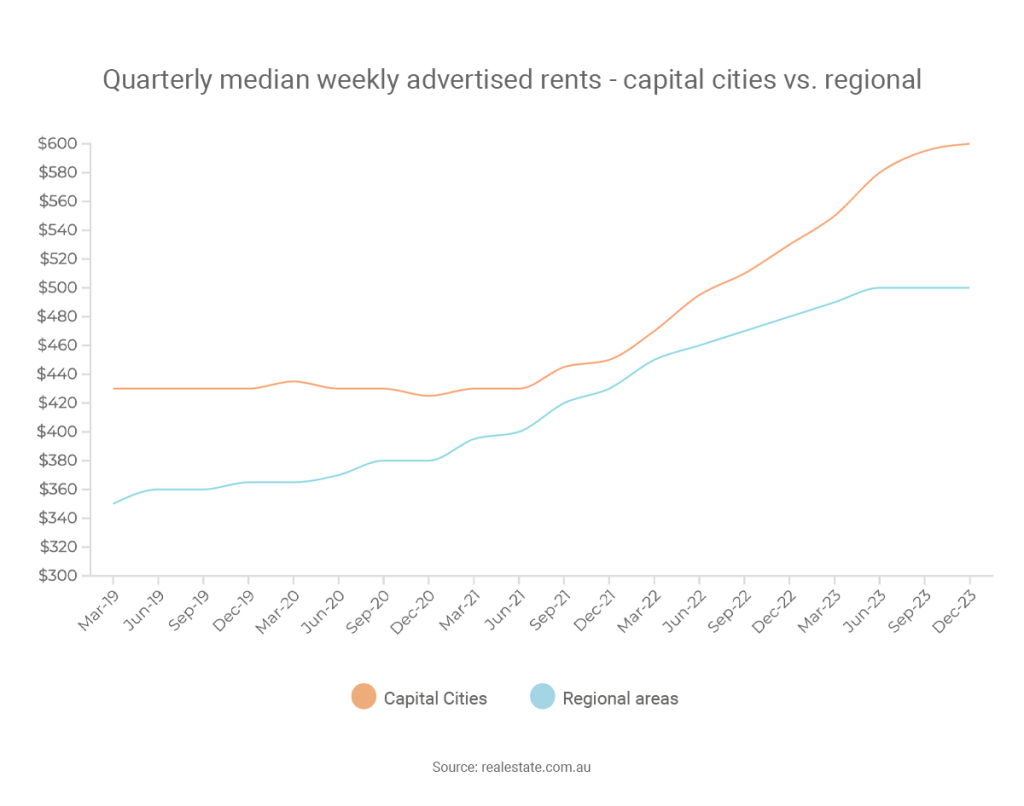

Why rents are expected to keep rising

Rents have increased in most capital cities over the past year and are likely to continue rising throughout 2024, according to a leading property data expert.

Between the December quarters of 2022 and 2023, the median rent on realestate.com.au rose 11.5%. That included double-digit gains in Perth (20.0%), Melbourne (18.3%), Sydney (16.7%) and Adelaide (12.5%), as well as increases in Brisbane (9.1%) and Darwin (1.7%). By contrast, rents stagnated in Canberra (0.0%) and declined in Hobart (-4.8%).

During the same period, the vacancy rate fell from 1.3% to just 1.1%. With rents growing and vacancies falling, this is potentially a good time to be a property investor.

PropTrack’s director of economic research, Cameron Kusher, forecast that the “tough rental market conditions” would continue.

“We expect supply to remain tight and demand to stay strong, likely pushing rents higher,” he said.

“Lending to investors trended higher over 2023, indicating that investors are returning to the housing market. However, many investors continued to sell, resulting in a relatively small pool of rental properties being available for the large number of people seeking accommodation. The rapid increase in Australia’s population exacerbated rental market challenges, as most people migrating to Australia become renters.”

If you are buying, re-financing or have any questions, contact me on the below information.

TAG Finance and Loans

TAG Finance and Loans

Sal Cinque | CEO

03 9886 0800 | loans@tagfinancial.com.au

Disclaimer: The information contained on this page is general in nature. Professional advice should be sought before acting on any aspect on this page. TAG Finance and Loans Pty Ltd ABN 25 609 906 863 Credit Representative Number 483873 National Mortgage Brokers Pty Ltd ABN 88 093 874 376 Australian Credit License 391209.